PREVIOUS

SPINNER Group Acquires RFS Broadcast IP

Motorola Solutions Achieves Record Q4 and Full-Year Sales and Earnings Per Share

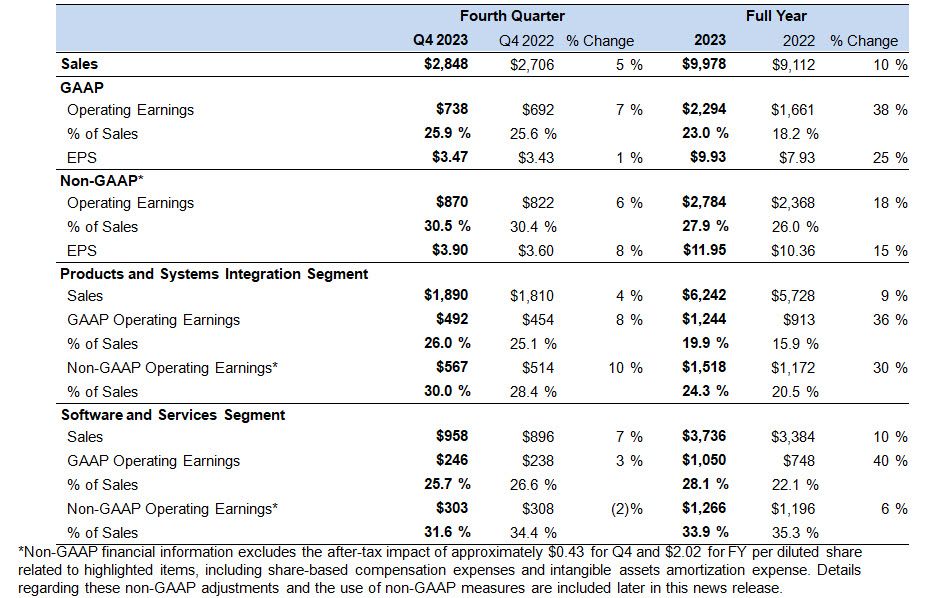

Sales of $2.8 billion, up 5% from Q4 in the prior year; up 10% for full year

Products and Systems Integration sales grew 4% in Q4; up 9% for full year

Software and Services sales grew 7% in Q4; up 10% for full year

Generated $1.2 billion of operating cash flow in Q4; $2.0 billion for full year, up 12%

GAAP Q4 earnings per share (EPS) of $3.47, up 1%; $9.93 for full year, up 25%

Non-GAAP Q4 EPS* of $3.90, up 8% versus a year ago; $11.95 for full year, up 15%

Ending backlog of $14.3 billion, inclusive of record Products and Systems Integration backlog

Announced $2.0 billion increase to the share repurchase authorization

Acquired IPVideo, creator of the HALO Smart Sensor

Motorola Solutions, Inc. (NYSE: MSI) today reported its earnings results for the fourth quarter and full year of 2023.

“2023 was an exceptional year, with record sales, earnings and operating cash flow,” said Greg Brown, Chairman and CEO of Motorola Solutions. “The strong growth we achieved reflects the continued robust demand for our safety and security solutions that help protect people, property and places. The momentum of our business is strong and I’m very pleased with our position for another year of revenue and earnings growth in 2024.”

KEY FINANCIAL RESULTS (presented in millions, except per share data and percentages)

OTHER SELECT FOURTH-QUARTER FINANCIAL RESULTS

Revenue - Fourth-quarter sales were $2.8 billion, up 5% from the year-ago quarter driven by growth in North America and International. Revenue from acquisitions was $17 million and the impact of favorable foreign currency rates was $16 million. The Products and Systems Integration segment grew 4% due to growth in land mobile radio (LMR) and video security and access control (Video). The Software and Services segment grew 7% driven by growth in Video, command center and LMR, inclusive of the reduction in Airwave revenue related to the pricing control in the United Kingdom’s Competition and Markets Authority’s (the “CMA”) remedies order.

Operating margin - GAAP operating margin was 25.9% of sales, up from 25.6% in the year-ago quarter. Non-GAAP operating margin was 30.5% of sales, up from 30.4% in the year-ago quarter. The increase in both GAAP and non-GAAP operating margin was primarily driven by higher sales and lower direct material costs, partially offset by the revenue reduction for Airwave.

Taxes - The GAAP effective tax rate was 15.7%, up from 11.0% in the year-ago quarter driven primarily by higher benefits in the prior year related to a partial release of a valuation allowance recorded on the U.S. foreign tax credits carryforward. The non-GAAP effective tax rate was 20.3%, down from 21.2% in the year-ago quarter, driven by higher benefits from stock-based compensation in the current year.

Cash flow - Operating and free cash flow were both $1.2 billion during the quarter driven by higher earnings and partially offset by higher cash taxes.

Capital allocation - During the quarter, the company paid $146 million in dividends, repurchased $117 million of its common stock and incurred $81 million in capital expenditures. Additionally, the company closed the acquisition of IPVideo, creator of the HALO Smart Sensor, for $170 million in cash, net of cash acquired.

OTHER SELECT FULL-YEAR FINANCIAL RESULTS

Revenue - Full-year sales were $10.0 billion, up 10% driven by growth in North America and International. The Products and Systems Integration segment grew 9% driven by higher sales of LMR and Video. The Software and Services segment grew 10% driven by growth in LMR services, command center and Video, partially offset by the revenue reduction for Airwave. Revenue from acquisitions was $98 million and the impact of unfavorable foreign currency rates was $38 million.

Operating margin - For the full year, GAAP operating margin was 23.0% of sales, compared to 18.2% for the prior year. The increase was primarily driven by lower direct material costs, higher sales, the $147 million fixed asset impairment charge related to the exit from the Emergency Services Network ("ESN") services contract in the U.K. recorded in the prior year and lower intangible amortization expense in the current year, partially offset by the revenue reduction for Airwave. Non-GAAP operating margin was 27.9% of sales, up from 26.0% in the prior year, driven by lower direct material costs, higher sales and improved operating leverage, partially offset by the revenue reduction for Airwave, higher employee incentives, higher expenses associated with acquired businesses and mix.

Taxes - The 2023 GAAP effective tax rate was 20.1%, up from 9.8% in the prior year driven primarily by a discrete deferred tax benefit recognized in 2022 as a result of an intra-group transfer of certain intellectual property rights. In addition, the company generated higher benefits in the prior year from a partial release of the valuation allowance recorded on the U.S. foreign tax credit carryforward and higher stock-based compensation. The non-GAAP effective tax rate was 21.9%, up from 20.1% in the previous year, primarily driven by lower benefits from stock-based compensation in the current year.

Cash flow - The company generated $2.0 billion in operating cash flow, up 12% versus the prior year. Free cash flow was $1.8 billion, up 14% versus the prior year. The increase in both operating and free cash flow was primarily driven by higher earnings generated in the current year partially offset by higher cash taxes.

Capital allocation - In 2023, the company repurchased $804 million of its common stock at an average price of $278.56 per share and paid $589 million in dividends. Additionally, the company closed the acquisition of IPVideo, creator of the HALO Smart Sensor, for $170 million in cash, net of cash acquired.

Backlog - The company ended the year with backlog of $14.3 billion, down $88 million from the prior year. Products and Systems Integrations segment backlog was up 2% or $93 million driven by continued strong demand in North America. Software and Services segment backlog was down 2% or $181 million, driven by the reduction related to the Airwave price control and revenue recognition for Airwave and ESN, partially offset by growth in multi-year software and services contracts in both North America and International and $113 million of favorable foreign currency rates.

NOTABLE WINS & ACHIEVEMENTS IN Q4

Software and Services

$330M+ LMR managed services renewal through 2034 for Denmark’s nationwide public safety communications network

$48M command center order for the City of Chicago Office of Public Safety Administration

$20M LMR service agreement for Spokane Regional Emergency Communications, WA

$19M mobile video order for a U.S. customer

$10M command center order for the City and County of San Francisco, CA

Products and Systems Integration

$90M P25 system and devices order for a U.S. customer

$67M P25 device order for Emergency Services Telecommunications Authority (ESTA) in Australia

$57M P25 APX NEXT devices order for U.S. customer

$38M P25 system order for the State of Arizona Department of Public Safety

$31M TETRA system order for a European customer

$13M fixed video order for an International customer

BUSINESS OUTLOOK

First-quarter 2024 - The company expects revenue growth of approximately 8% compared to the first quarter of 2023. The company expects non-GAAP earnings per share in the range of $2.50 to $2.55 per share. This assumes approximately 172 million fully diluted shares and a non-GAAP effective tax rate of approximately 23%.

Full-year 2024 - The company expects revenue growth of approximately 6% and non-GAAP earnings per share in the range of $12.62 to $12.72 per share. This assumes approximately 171 million fully diluted shares and a non-GAAP effective tax rate between 23% and 24%.

The company has not quantitatively reconciled its guidance for forward-looking non-GAAP measurements in this news release to their most comparable GAAP measurements because the company does not provide specific guidance for the various reconciling items as certain items that impact these measures have not occurred, are out of the company’s control, or cannot be reasonably predicted. Accordingly, a reconciliation to the most comparable GAAP financial measurement is not available without unreasonable effort. Please note that the unavailable reconciling items could significantly impact the company’s results.

RECENT EVENTS

CMA UPDATE

In October 2021, the CMA announced that it had opened a market investigation into the Mobile Radio Network Services market. This investigation included Airwave, the company’s private mobile radio communications network that it acquired in 2016. Airwave provides mission-critical voice and data communications to emergency services and other agencies in Great Britain.

In early 2023 the CMA issued its final decision which stated it will impose a prospective price control on Airwave. The company strongly disagreed with the CMA’s final decision and it filed an appeal with the Competition Appeal Tribunal ("CAT"). On July 31, 2023, the CMA adopted a remedies order which implemented the price control set out in its final decision, which was suspended until the CAT dismissed the company's appeal on December 22, 2023. The company has until February 14, 2024 to file an application with the United Kingdom Court of Appeal requesting that it hear the company's appeal.

Based on the adoption of the remedies order, since August 1, 2023, revenue under the Airwave contract has been recognized in accordance with the prospective price control. As the company's appeal to the CAT has been dismissed, revenue will continue to be recognized according to the remedies order published by the CMA, unless the United Kingdom Court of Appeal were to reverse the remedies order. The company's backlog for Airwave services contracted with the United Kingdom Home Office through 2026, inclusive of the five month period beginning August 1, 2023, was reduced by $777 million to align with the remedies order as of December 31, 2023.

MACROECONOMIC EVENTS

During fiscal year 2023, the company operated under market conditions influenced by events such as those discussed below. For a further discussion of the risks the company encounters in its business, please refer to Part I. Item 1A. “Risk Factors” in the company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022 and Part II. Item 1A. “Risk Factors” in the company’s Quarterly Report on Form 10-Q for the fiscal quarter ended September 30, 2023.

In 2023, the company experienced improved conditions with respect to availability of materials in the semiconductor market. The company reduced its inventory carrying levels as compared to 2022 in response to the improved supply conditions. The company continues to remain focused on improving its supplier network, engineering alternative designs and working to reduce supply shortages and effectively manage costs. In addition, the company continues to actively manage its inventory by diversifying the footprint of its supply chain operations, including by finalizing a strategic agreement relating to the company's video manufacturing operations during the first quarter of 2024, and maintaining increased levels of inventory in targeted areas to support increased demand and customer requirements.

Continue to read the full finance results